Last week I watched a mom at Costco completely reorganize her cart three times. Not because she forgot something—she was doing real-time math on whether the bulk paper towels made sense when gas to get there now costs $18 roundtrip versus the $11 it was last year.

Reuters reported that consumer confidence dropped in late May as families watched their grocery bills climb while gas prices stayed stubbornly high heading into summer. This isn't just about tighter budgets. When your core operating costs jump 15-25%, every single routine in your household starts breaking down.

The mom at Costco? She ended up leaving without the paper towels. But more importantly, she texted her husband to cancel their youngest's extra swim lessons for June. That's how family budget inflation actually plays out—not in spreadsheets, but in dozens of micro-decisions that cascade through your entire household system.

The hidden operational crisis nobody talks about

Most families don't realize they're running a complex operation until inflation forces them to see it. You've got recurring payments hitting at different times, variable costs that fluctuate wildly week to week, multiple people making spending decisions independently, and kids who don't understand why suddenly the answer to everything is "we'll see."

A family I worked with recently discovered they were essentially running three separate financial systems—mom's mental tracking of groceries and kids' activities, dad's credit card for gas and hardware store runs, and a checking account that nobody really monitored closely. When costs jumped, their informal system completely collapsed.

The real problem isn't the higher prices. It's that most household systems were built for stability. They assume gas costs roughly the same each month, grocery bills stay within a predictable range, and you can plan summer activities in March without worrying about whether you can afford them by June.

Your coordination problem just became a math problem

When inflation hits a typical household, the grocery shopping routine that worked when milk was $3.50 doesn't work at $5.20. Not because you can't afford the extra $1.70, but because that same increase hits 40 other items, and suddenly your weekly shop is $65 more expensive. Now someone needs to shop at two stores to find deals, which burns more gas, which means coordinating who has the car when.

Kids' activities get complicated fast. Dance class is prepaid through June, but basketball camp wants $400 by next week. Swimming lessons auto-renew monthly. Each kid assumes their thing is safe while parents scramble to figure out which commitments they can actually keep. Nobody wants to be the bad guy who cancels something.

The household division of labor stops making financial sense. Maybe you've been paying $120 monthly for biweekly cleaning. When that feels like too much, someone needs to take over those hours. But who? And when? The teenager who could help has a summer job precisely because the family needs extra income.

Stop pretending this is temporary

Families keep waiting for things to "go back to normal." They make temporary cuts, assuming in a month or two they can resume regular programming. This thinking creates operational chaos.

Stop losing track of household duties.

Famioly helps you organize, assign & complete family tasks efficiently.

- Centralized task management

- Shared family calendar

- Budget & expense tracking

No credit card required

-

Week 1

"We'll just eat out less this month"

-

Week 2

Someone forgets to pack lunch, grabs takeout, feels guilty

-

Week 3

Overcorrect by buying $300 of Costco groceries that don't quite work for actual meals

-

Week 4

Give up, order pizza, promise to "start fresh" next month

The operational reality is that sustained high gas prices mean every single trip needs reconsideration. Not just vacation plans—I mean the Tuesday afternoon Target run, the Saturday morning sports shuttling, the "quick" stop at three different stores to find the specific yogurt your toddler will actually eat.

Build new systems, don't patch old ones

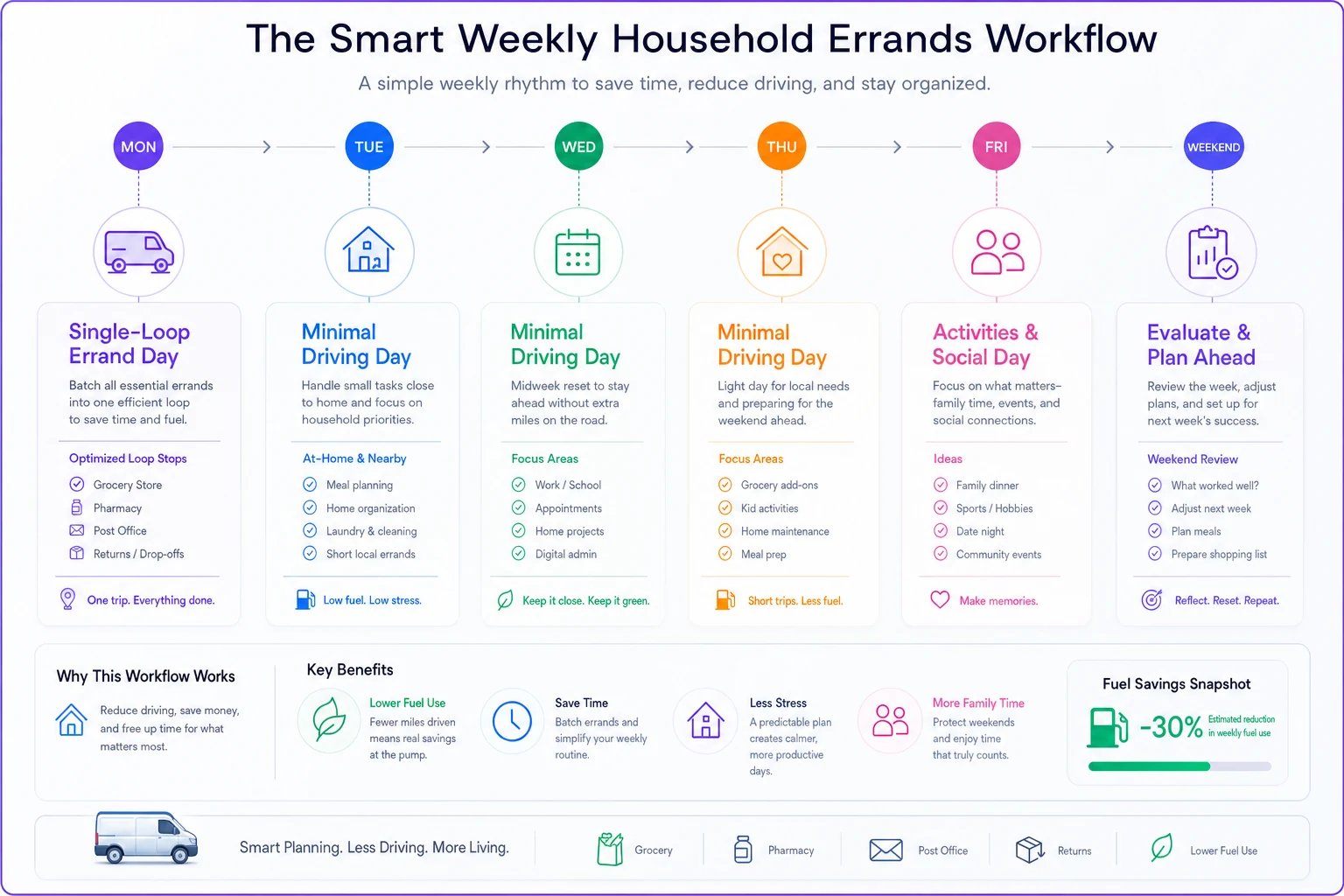

A family in my neighborhood restructured their entire week around gas prices. Sounds dramatic, but it worked:

Monday became "errand day"—one parent takes the van, hits grocery store, pharmacy, post office, and any returns in a single loop. Tuesday through Thursday, nobody drives unnecessarily. Friday is activities and social stuff. Weekends they evaluate if plans are worth the gas.

Here's a simple visual of that weekly loop.

Before this system: ~$280/month in gas across two vehicles

After: ~$195/month

But what matters more—they stopped having daily negotiations about who needs the car. The stress reduction was worth more than the $85 savings.

The three-account solution most families need right now

Your current shared account system is probably some version of "everything goes in, bills come out, hopefully there's money left." This breaks catastrophically when costs spike unexpectedly.

Switch to this:

Account 1: Fixed costs only Mortgage/rent, insurance, car payments, subscriptions. Nothing else touches this account. Fund it with exactly what's needed plus 5%. When inflation hits, this account stays stable.

Account 2: Variable operations Groceries, gas, utilities, kids' immediate needs. This gets funded weekly, not monthly. When costs spike, you adjust week by week, not in huge painful monthly reconciliations.

Account 3: Discretionary buffer Everything else. Eating out, entertainment, non-essential kids' activities. This account shrinks first when things get tight. Everyone can see exactly how much "fun money" exists in real-time.

Automate the weekly transfer to Account 2 the day after payday so household operations are funded consistently.

One family implemented this after their shared account system kept causing confusion about what they could actually afford. Within three weeks, the daily money stress disappeared even though their costs hadn't decreased.

Renegotiate everything (here's the script that works)

Families assume their fixed costs are actually fixed. They're not. Nearly every recurring charge can be adjusted when you approach it correctly.

Don't call saying "times are tough, can you help?" Instead, use this operational approach:

"Hi, I'm reviewing our household services for the next quarter. We've been customers for [timeframe] and pay [amount] monthly. I need to either reduce this to [target amount] or put the service on hold for July and August. What options can you offer to keep us active?"

Results from families using this approach:

-

Lawn service

Switched from weekly to biweekly, saved $110/month

-

Internet

Downgraded speed tier nobody noticed, saved $30/month

-

Streaming services

Paused three for summer, saved $45/month

-

Kids' tutoring

Moved to every-other-week for summer, saved $200/month

That's $385/month recovered without canceling anything permanently.

The vendor conversation nobody wants to have

Your house cleaner, babysitter, lawn service—these people depend on your business. Having an honest operational conversation helps everyone.

"We need to adjust our service schedule for the summer. Instead of weekly, could we move to monthly deep cleans? Or would you prefer we pause until September and resume the regular schedule then?"

Most service providers prefer keeping some income over losing clients entirely. A family I know worked out a deal where their cleaner comes monthly for deep clean at the same total monthly cost as biweekly basic cleaning. Everyone wins—family saves money, cleaner keeps consistent income.

Create your 72-hour spending freeze protocol

When costs spiral, families need circuit breakers. Not month-long austerity measures nobody can maintain, but short tactical pauses that stop the bleeding.

The 72-hour freeze works like this:

Hour 0-24: No spending except true emergencies. Gas tank on E? That's an emergency. Kid wants McDonald's? Not an emergency.

Hour 24-48: List everything you wanted to buy but didn't. Calculate the total. That's your immediate savings.

Hour 48-72: Evaluate the list. What was actually needed? What was impulse? Buy only the true needs.

A family of five tried this after a particularly expensive week. Their 72-hour "wanted but didn't buy" list totaled $340. After evaluation, they spent $87 on actual needs. The rest was noise—Amazon impulses, convenience food instead of cooking, random Target items.

The summer schedule shuffle that saves thousands

Summer breaks most family budgets because the operational tempo completely changes. No school means entertainment costs. No free lunch means more grocery spending. Camps cost hundreds per week per kid.

The shuffle that works:

Week classification system:

-

A weeks

One major paid activity or camp

-

B weeks

Free activities only (library, park, playdates)

-

C weeks

Work-from-home weeks where kids entertain themselves

Pattern: A-B-C-B-A-C-C-B-A

| Scenario | Estimated Cost |

|---|---|

| Traditional summer (camps/activities most weeks) | ~$4,200 |

| Shuffle system | ~$1,400 |

The saved $2,800 covers a lot of inflated grocery bills.

Make kids part of the operation

Stop protecting kids from household financial operations. They need to understand why routines are changing.

-

8-year-old

"You have $200 for all summer activities. Here's the list with prices. What do you choose?"

-

12-year-old

"Your monthly budget is $75. That covers your activities and wants. You manage it."

-

16-year-old

"Here's a gas card with $100/month. When it's empty, you're walking or finding rides."

Watch how quickly kids become operational thinkers when they own their piece of the puzzle.

The meal planning system that actually survives inflation

Every family tries meal planning. Most quit within two weeks because the system is too rigid. When chicken breast jumps from $3.99/lb to $7.99/lb, your carefully planned Tuesday dinner becomes a budget crisis.

Build flexibility into the system:

Protein rotation based on sales:

-

Under $3/lb

Stock up week

-

$3-5/lb

Normal purchases

-

Over $5/lb

Vegetarian week

The reliable fifteen:

-

Spaghetti with meat sauce (~$9)

-

Bean and cheese quesadillas (~$7)

-

Breakfast for dinner (~$8)

-

Tuna noodle casserole (~$8)

-

Grilled cheese and tomato soup (~$6)

Not gourmet, but sustainable. And when hamburger meat hits $7/lb, you're not standing in the store recalculating your entire week.

Build your financial fire drill protocol

Families practice fire drills but never practice financial emergencies. When inflation accelerates or someone's hours get cut, you need muscle memory, not panic decisions.

Run this drill quarterly:

Day 1: Cut spending to absolute essentials only. Track everything.

Day 7: Review what you actually spent versus normal week.

Day 8: Identify what was truly painful to cut versus what nobody missed.

A family discovered during their drill:

-

Nobody missed the three streaming services they paused

-

Skipping Starbucks saved $47 in a week

-

Cooking every meal saved $130 but burned everyone out

-

The kids didn't notice when name-brand snacks became generic

This intelligence becomes your playbook when real pressure hits.

When automation becomes essential, not optional

At a certain point, manual tracking and coordination breaks. You can't spreadsheet your way through volatile inflation while managing three kids' schedules and two working parents.

Smart families are building operational systems that handle the complexity automatically. Not fancy AI necessarily, but practical automation that removes decision fatigue.

Examples that work:

-

Automatic bill pay for true fixed costs only

-

Spending trackers that alert when categories exceed limits

-

Shared calendars that show when major expenses hit

-

Shopping lists that update based on inventory

The goal isn't perfection. It's reducing the daily negotiation and mental overhead that inflation creates. When your system handles the basics, you can focus on the strategic decisions that actually matter.

Your next 48 hours

Right now, before next week's bills hit:

-

Run your three-account setup. Move money today.

-

Call three service providers. Use the script.

-

Set your first 72-hour freeze for this weekend.

-

Give kids their summer numbers.

-

List your fifteen reliable meals.

The families succeeding right now aren't the ones with the most money. They're the ones who adapted their operations fastest. While others wait for inflation to reverse, they've built systems that work regardless.

That mom from Costco? I saw her last week. She'd switched to shopping at 6 AM on Tuesdays when the store is empty. One focused trip, list in hand, no kids arguing for extras. She saved twelve minutes and $60 just by changing her operational timing.

Your household is more resilient than you think. But resilience requires systems, not hope. The squeeze is real, but your response doesn't have to be reactive. Build the operations that match reality, not the reality you wish existed.

The difference between families who thrive and families who struggle through inflation isn't income. It's operational intelligence. Time to build yours.

Ready to simplify your household management?

Join thousands of families using Famioly to save time, reduce home management stress, and keep the household running smoothly.