My neighbor Sarah knocked on my door last month holding a credit card statement and looking like she'd discovered her husband was living a double life. "He spent $400 on golf equipment," she said. "Without telling me."

Her husband Mike makes $85,000 a year. They have no debt. Their kids' college funds are on track. But that $400 purchase nearly started World War III in their kitchen because they'd never actually decided: what spending requires a conversation?

After building financial tracking systems for dozens of small businesses, I noticed something. Most households operate with vaguer financial rules than a corner pizza shop. A pizza place has clearer spending authority ($50 for supplies without asking the owner) than most families managing $150,000 in annual cash flow.

The mess in household finances isn't about budgets or tracking apps. It's about having zero actual systems for decisions, timing, and authority. You wouldn't run a business where every partner could spend freely from the main account with no discussion threshold. Yet that's exactly how most households operate.

Why household money systems fail at the worst moments

Every household starts with good intentions. Joint checking account, maybe separate credit cards, loose agreement about "big purchases." Then reality hits around month three.

Someone buys a $200 espresso machine ("for both of us"). Someone else books a $500 weekend trip with friends ("I mentioned it last month"). The car needs $1,400 in repairs the same week property taxes are due. Suddenly you're having heated discussions about whether gym memberships count as personal or household expenses while your actual financial planning gets pushed to "next quarter" indefinitely.

The breakdown happens in stages. Couples start with weekly money dates. Those become monthly. Then quarterly. Then only during tax season or after a financial shock. Meanwhile, spending decisions happen daily with no framework, creating a backlog of unresolved financial resentments.

Household financial systems are fragile because they mix operational and emotional components. In a business, if someone overspends their department budget, it's a process violation. In a household, if someone overspends their "fun money," it becomes a trust issue. Every financial hiccup turns into a relationship stress test.

Add kids and the coordination problem multiplies. Now you're managing allowances, teaching money lessons, tracking school expenses, sports costs, and trying to model good financial behavior while your own system consists of "check the bank balance and hope for the best."

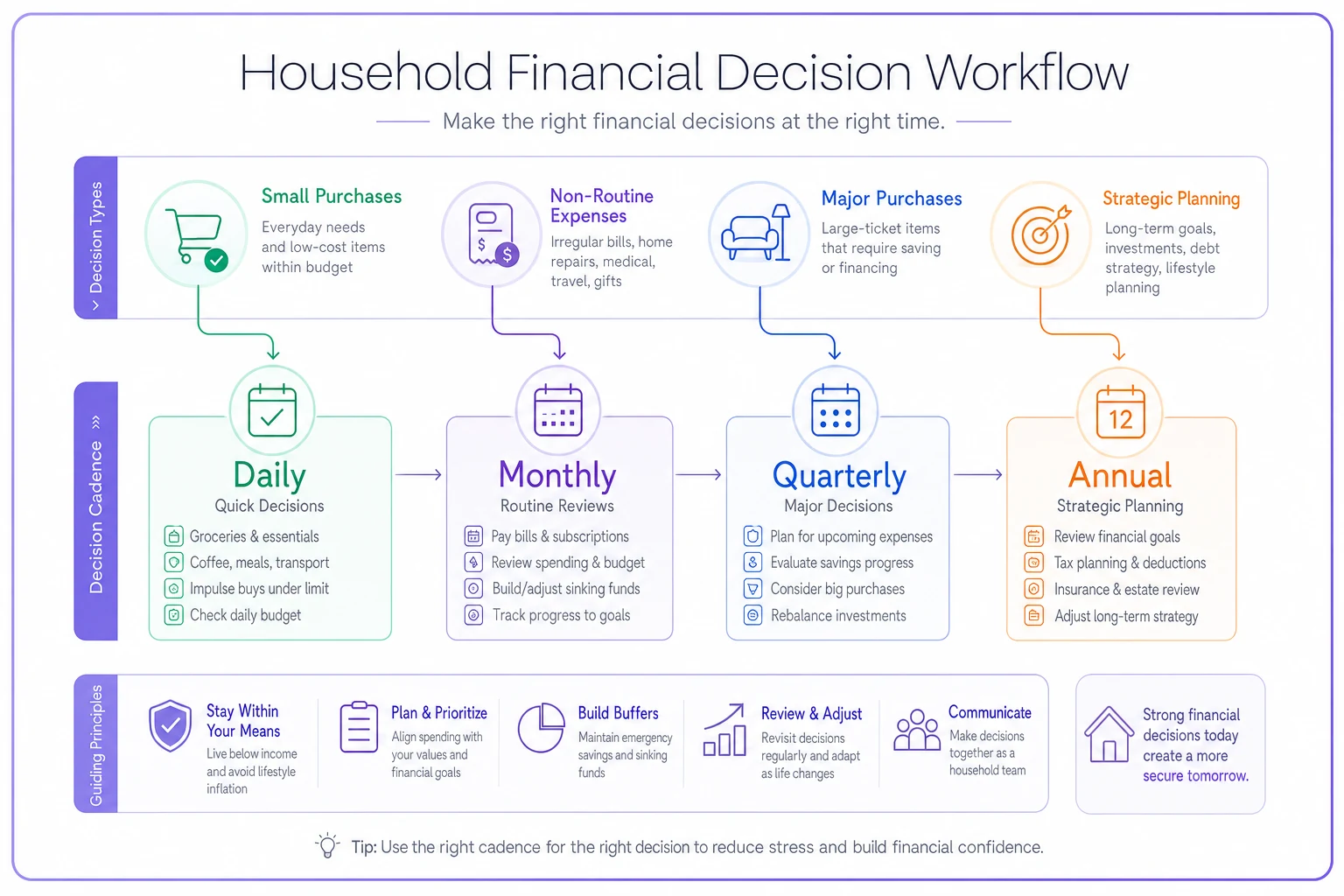

The three-tier cadence that actually works

After watching hundreds of small businesses establish expense approval workflows, I started applying the same operational thinking to household finances. The key isn't more frequent discussions - it's having the right discussion at the right interval.

Stop losing track of household duties.

Famioly helps you organize, assign & complete family tasks efficiently.

- Centralized task management

- Shared family calendar

- Budget & expense tracking

No credit card required

Daily Operations (No Discussion Needed)

-

Groceries under $150

-

Gas and routine transportation

-

Recurring subscriptions already approved

-

Kids' school lunches and small needs

-

Personal spending within set limits

Monthly Reviews (30-minute sync)

-

Review last month's spending categories

-

Check progress on savings goals

-

Approve any upcoming non-routine expenses over $200

-

Adjust next month's personal spending limits if needed

-

Quick scan for subscription creep

Quarterly Planning (2-hour session)

-

Review investment and retirement contributions

-

Plan major purchases for next quarter

-

Adjust household vs personal spending rules

-

Set or modify kids' allowance and learning goals

-

Evaluate if current system is working

Annual Strategy (half-day workshop)

-

Set next year's financial goals

-

Renegotiate personal vs household boundaries

-

Plan major expenses (vacation, home improvements)

-

Review insurance and investment allocations

-

Teach kids about the family's financial values

Here's a simple workflow you can visualize to map decision types to meeting cadences.

The magic happens when everyone knows which decisions belong at which level. No more asking permission for a $30 book (daily operations). No more surprise $500 purchases (requires monthly approval). No more discovering in December that you've been saving for different goals all year (quarterly alignment).

Personal vs shared: the decision matrix nobody talks about

Most couples never explicitly decide: what expenses are "ours" versus "mine"? Without clear rules, every purchase becomes a potential argument.

Having actual formulas changes everything. One family uses: Shared contribution = 70% of income, Personal retention = 30% of income. Higher earner contributes proportionally more to shared, but everyone keeps the same percentage for personal.

| Category | Shared Account | Personal Account | Decision Rule |

|---|---|---|---|

| Housing | Mortgage, utilities, repairs | Room decorations under $100 | Infrastructure = shared, aesthetics = personal |

| Food | Groceries, family dinners | Work lunches, coffee runs | Family meals = shared, individual consumption = personal |

| Transportation | Car payments, insurance, gas for family trips | Commute gas, personal trip gas | Family asset = shared, individual use = personal |

| Health | Insurance, medical bills, gym family membership | Boutique fitness classes, supplements | Required = shared, optional = personal |

| Kids | School, clothes, activities, college savings | Gifts from personal funds | Needs = shared, wants from personal gifts = personal |

| Entertainment | Family vacations, shared streaming | Individual hobbies, nights out with friends | Together = shared, separate = personal |

Another couple does it differently: Fixed shared contribution ($4,000/month each), everything else is personal. When one got a raise, their personal fund grew but shared contribution stayed flat.

The worst system is no system - where every expense requires negotiation. "Is this haircut a personal expense or household maintenance?" shouldn't be a recurring monthly debate.

Kids' allowances that teach operations, not just counting

Most allowance systems teach kids to count money. But operational allowance systems teach them how financial systems actually work.

Traditional allowance: $10 per week, save some, spend some. Kid learns money exists. That's about it.

Operational allowance looks different:

-

Age 5-8

Introduction to Systems

- $5 base weekly allowance - Extra $1 for completing "household operations" checklist - Must track in simple ledger (drawing pictures counts) - Monthly "board meeting" to report on spending -

Age 9-12

Department Management

- $20 monthly base budget - Manages one household category (pet supplies, family snacks) - Must stay within budget and handle procurement - Quarterly performance bonus based on managing well -

Age 13-16

Profit Center Operations

- $50 monthly base - Can earn more by taking on household services (lawn, tech support) - Must "bid" on family projects against parents doing it - Manages own clothing budget within parameters -

Age 16+

Full Financial Operations

- Access to family financial planning meetings - Manages significant category (own car expenses, sports costs) - Participates in quarterly planning - Learns investment basics with real money

One family implemented this after their business-owning friends complained their kids had no idea how the family business actually worked. Their 14-year-old now manages the family's streaming subscriptions - researching options, canceling unused services, finding family plan deals. She saved them $65 per month and earned a 20% "management fee" on savings generated.

When the 11-year-old forgot to buy dog food with the pet supply budget, the consequence was immediate and visible. When the 16-year-old found a better phone plan, the whole family benefited.

The spending authority ladder most families never create

In business, everyone knows their spending authority. The office manager can buy supplies up to $200. The department head can approve up to $2,000. Households need the same clarity.

The friction should match the impact. Buying lunch shouldn't require committee approval. Buying a new laptop shouldn't be a surprise discovery on the credit card statement.

-

Level 0

Automatic (No approval needed)

- Under $50 personal spending - Regular groceries and household supplies - Approved recurring expenses - Emergency medical needs -

Level 1

Notify (Spend then inform)

- $50-$200 personal spending - Household items under $200 - Kids' urgent school needs - Minor car maintenance -

Level 2

Quick Check (Text or quick conversation)

- $200-$500 either account - Non-urgent kid activities - Annual subscriptions - Social commitments involving both -

Level 3

Discussion Required (Sit-down conversation)

- $500-$2,000 from any account - New recurring expenses - Changes to savings rate - Kids' major activities or equipment -

Level 4

Planning Session (Scheduled meeting)

- Over $2,000 purchases - Investment changes - Major household projects - Anything affecting annual goals

Families get into trouble when these levels aren't clear. I watched one couple argue for 20 minutes about whether a $180 vacuum cleaner needed approval. Neither remembered what they'd agreed their threshold was. Meanwhile the old vacuum was broken for three weeks because nobody wanted to make the decision.

What breaks when you scale from couple to family

A couple can wing it with loose financial agreements. Add kids and the operational complexity multiplies. Not just more expenses - more decision makers, more accounts, more teaching moments, more competing priorities.

Scaling breaks happen predictably.

First kid arrives. Suddenly you're tracking daycare, diapers, doctor visits. The "we'll just split everything" approach creates constant reconciliation work. Who pays for formula at 2 AM becomes an actual operational problem.

Second kid hits different ages. Now you're managing different allowance tiers, different activity costs, fairness questions. The 12-year-old wants to know why the 8-year-old's gymnastics costs more than their art classes. Without clear policies, every comparison becomes a negotiation.

Teenagers enter the scene. They need money for social activities, want expensive gear for sports, start thinking about cars. Your simple "here's your allowance" system can't handle the complexity.

Multiple income streams appear. One spouse gets a bonus. The other starts a side business. Kid gets a part-time job. The "everything goes in one pot" system stops making sense when different people are contributing different amounts at different times.

The families that successfully scale have one thing in common: they add structure before they need it. They create the Level 2 spending authority before they have the argument about the surprise purchase. They set up the quarterly planning rhythm before they realize they're working toward different goals.

Building your household's financial operating system

The transformation from financial chaos to smooth operations doesn't require complicated software. It requires deciding your rules and cadences, then actually following them.

Start with the monthly sync. Pick the first Sunday of each month. Order takeout so nobody's cooking. Take 30 minutes to review last month and approve next month's known expenses over $200. Don't try to solve every financial question - just establish the rhythm.

Next, define your shared versus personal split. Pick actual numbers. If you make $60,000 and your partner makes $90,000, decide: does each contribute the same amount to shared expenses, or the same percentage? There's no right answer, only the answer you both agree to follow.

Create your spending authority ladder. Write it down. Put it on the fridge.

When someone inevitably breaks it, treat it as a system update need, not a trust violation. Maybe $200 is too low for Level 2. Adjust and continue.

For kids, start wherever they are. A 7-year-old can manage buying fruit snacks for school lunches within a $20 monthly budget. A 15-year-old can research and recommend the family's next cell phone plan. The point isn't perfection - it's giving them real operational experience with real consequences.

The quarterly planning sessions feel excessive until you do them. That's when you catch the subscription you forgot to cancel, the savings goal you've been ignoring, the investment account that should be rebalanced. Two hours every three months prevents twelve months of financial drift.

Common failure points and system adjustments

Even good systems break. The difference between households that succeed and those that don't isn't having perfect systems - it's recognizing when the system needs adjustment.

The monthly meeting gets skipped because someone's traveling. Fine. But if you skip two months in a row, the system's breaking. Either the cadence is too frequent or the meeting's too long. Cut it to 15 minutes or move it to every six weeks, but don't let it disappear entirely.

Personal spending limits feel unfair when income changes. Someone gets a raise or loses hours. The 70/30 split that worked when you both made similar amounts feels wrong when there's a big gap. Time to renegotiate the formula, not abandon the system.

Kids game their allowance system. They rush through household tasks to get paid but do them poorly. Or they negotiate every purchase to come from the shared account instead of their personal money. These aren't system failures - they're kids learning to work within systems. Add quality metrics or clarify the boundaries.

The "quick check" for $200-$500 purchases becomes rubber-stamp approval. Every text gets a "sure, go ahead" response. Either your limit's too low and should move to $350, or you need to add more structure to the quick check - maybe a photo of what's being bought or a one-sentence justification.

The difference between planning and operating

Most household finance advice focuses on planning. Make a budget. Set goals. Track net worth. But planning without operations is like having a beautiful business plan with no actual business.

Operations means having an answer when your kid needs $40 for a school field trip tomorrow. Not "let me check the budget" but "field trips come from the education fund, here's the money."

Operations means both partners can grocery shop without conference-calling about every purchase. The rules are clear: regular groceries from shared account, fancy cheese for your book club from personal account.

Operations means your teenager knows exactly how to get money for gas. They submit their miles to the monthly meeting, get reimbursed at 30 cents per mile for agreed-upon trips, and pay for personal trips themselves. No daily negotiations about "can I have $20 for gas?"

The shift from planning to operating changes everything. Instead of having the same money arguments monthly, you have system refinement discussions quarterly. Instead of surprising each other with purchases, you surprise each other with how smoothly the money flows.

Building operational knowledge, not just saving money

The real goal isn't maximizing every dollar - it's building a household where everyone understands how money operations work.

Your 12-year-old who manages the streaming service budget will understand departmental budgets when they enter the workforce. Your partner who knows exactly when to check versus when to just spend will be a better collaborator in every aspect of life.

Traditional financial advice creates savers and spenders. Operational financial systems create people who understand how money flows through organizations, how decisions compound, and how systems either enable or constrain growth.

When your kid takes their first job, they'll understand why the store manager can't just give them a raise tomorrow - there's a system, a budget cycle, an approval chain. When they start their first business or join a startup, they'll understand why runway matters more than revenue in the early days.

More immediately, they'll understand why you can't just "find" $500 for the cool camp their friend is attending. Not because you're mean or broke, but because that money is already allocated in the system and pulling it means something else doesn't happen.

This understanding changes behavior. Kids stop asking for money and start proposing budget adjustments. Partners stop questioning purchases within agreed limits and start optimizing the system itself.

From financial chaos to operational clarity

Sarah and Mike, my neighbors with the $400 golf club crisis? They implemented a simple system. Personal spending under $100: no discussion. $100-$300: text the amount and what it's for. Over $300: actual conversation. Their fights about money dropped to nearly zero in two months.

The bigger change was operational. They stopped having to think about every purchase. The decision tree was clear. The monthly meeting was scheduled. The quarterly planning happened whether they felt like it or not.

Their 13-year-old son now manages his own sports equipment budget. He learned to buy used cleats in August for fall soccer instead of waiting until the season started when everything's full price. That's not just saving money - that's understanding operations.

The best household financial systems aren't the most detailed or restrictive. They're the ones that actually get followed because they match how your household operates. Start with a basic cadence and a simple sharing rule. Add complexity only when the simple system breaks.

Your household is already a complex financial operation. You're managing multiple income streams, dozens of expense categories, various saving goals, and trying to teach the next generation about money. You might as well have an actual system for it.

The families that thrive financially aren't necessarily the ones that earn the most. They're the ones that operate the smoothest. Where everyone knows the rules, follows the cadence, and understands their authority. Where money discussions are about optimizing the system, not relitigating every purchase.

Stop running your household finances like it's a continuous negotiation. Start running them like the operational system they need to be.

Ready to simplify your household management?

Join thousands of families using Famioly to save time, reduce home management stress, and keep the household running smoothly.