Irregular income creates a specific operational problem most financial advice completely misses. You can't just "budget better" when your paychecks swing from $2,800 one month to $6,400 the next. Standard advice about automated bill pay and monthly budgeting breaks down when income arrives unpredictably.

Working with freelancers, contractors, and commission-based workers shows the same pattern: households with variable income need different financial operations than those with steady paychecks. Not more discipline. Not better budgeting apps. Different workflows entirely.

The gap between how financial systems are designed and how irregular income actually works creates unnecessary stress for millions of households. Banks assume steady deposits. Bill collectors expect consistent payment dates. Budget templates require predictable income. Meanwhile, real families navigate feast-or-famine cycles with systems built for corporate employees.

Why standard bill management fails on variable income

Traditional bill payment assumes income arrives before bills are due. Set up autopay on the 5th, get paid on the 1st, everything flows smoothly. This breaks immediately when a client pays 45 days late or commission checks arrive whenever corporate accounting gets around to it.

The mismatch shows up in predictable ways. A freelance designer gets three project payments in November, nothing in December, then scrambles to cover January rent. A real estate agent closes two deals in spring, lives carefully through summer, then panics when property tax arrives in fall. A rideshare driver earns $900 one week, $400 the next, never knowing which bills can get paid when.

Banks make this worse by processing everything in order received. Your mortgage autopay hits Monday morning, overdrafts because Friday's deposit hasn't cleared, triggering a $34 fee plus a late payment mark. The bank reverses the fee after three phone calls, but the credit report damage remains.

Most households try fixing this with credit cards, creating a different problem. Floating bills on cards during slow periods, paying them off during good months, slowly accumulating interest when timing doesn't align. What starts as a bridge becomes permanent debt.

Build your prioritized payment hierarchy

Operational clarity starts with explicit payment priorities. Not vague categories like "needs versus wants" but specific vendor rankings based on real consequences.

Stop losing track of household duties.

Famioly helps you organize, assign & complete family tasks efficiently.

- Centralized task management

- Shared family calendar

- Budget & expense tracking

No credit card required

Your hierarchy reflects actual risk, not theoretical importance. Missing a Netflix payment suspends entertainment. Missing rent starts eviction proceedings. Missing car insurance creates legal liability. Missing internet kills your ability to earn. The operational impact determines the ranking.

Create three tiers based on consequence timing:

Tier 1: Immediate operational failure These payments protect your ability to function and earn. Housing (rent/mortgage), utilities keeping you operational (electric, water, internet if you work from home), transportation enabling work (car payment, insurance, gas money), and anything protecting your income source (professional licenses, required tools).

Tier 2: Degraded operations within 30 days These matter but offer buffer time. Health insurance (coverage continues briefly), non-critical utilities (gas heating in summer), minimum debt payments (avoiding default but not paying extra), basic food budget (beyond rice and beans).

Tier 3: Lifestyle maintenance Everything else. Streaming services, gym memberships, subscription boxes, dining budget, hobby expenses, accelerated debt payments, savings contributions.

The ranking changes based on your situation. A graphic designer ranks internet as Tier 1. A carpenter ranks it Tier 3. An Uber driver puts car insurance in Tier 1 while someone working from home might rank it Tier 2.

Calculate your survival number and operating buffer

Your survival number equals the monthly total of Tier 1 expenses. Calculate it precisely. Don't estimate "$2,000-ish" when the real number is $2,340. Include everything that would cause operational failure if missed.

Add irregular Tier 1 expenses converted to monthly amounts. Car registration costs $280 annually? That's $24 monthly. Professional insurance runs $1,400 yearly? Add $117 monthly. These hidden obligations destroy cash flow when they surprise you.

Convert annual irregular Tier 1 expenses to monthly amounts to avoid surprises.

Your operating buffer target equals three times your survival number. Not three months of full expenses. Three times the amount needed to keep functioning. For most households with a $2,400 survival number, that means maintaining $7,200 in checking before paying Tier 2 or 3 expenses.

This sounds impossible until you see the math work. A contractor maintaining a $7,200 buffer with a $2,400 survival number can weather a 10-week income gap without touching credit cards. The same contractor with no buffer hits credit cards by week three, accumulating interest that compounds the problem.

Match payment timing to income patterns

Standard advice says pay bills when due. Variable income households need different timing logic based on cash position.

| Buffer Level | Payment Strategy | Tier 1 | Tier 2 | Tier 3 |

|---|---|---|---|---|

| Above 3x survival (feast period) | Pay all tiers normally | Pay on schedule | Pay on schedule | Pay on schedule |

| 1x-3x survival (normal period) | Conservative approach | Pay immediately | Pay on schedule | Pause until buffer rebuilds |

| Below 1x survival (famine period) | Emergency mode | Pay only these | Negotiate delays | Cancel entirely |

The key: decide payment actions based on buffer level, not current income. A $5,000 check doesn't mean spending freely if your buffer sits below target. An empty week doesn't mean panic if your buffer remains healthy.

When buffer exceeds target, you can pay all three tiers on regular schedules, pay ahead on Tier 1 if vendors allow, and build additional buffer. But avoid lifestyle inflation in Tier 3.

When buffer sits between 1x and 3x survival, pay Tier 1 immediately upon income arrival, maintain Tier 2 on standard schedule, but pause Tier 3 until buffer rebuilds.

During famine periods below 1x survival, execute only Tier 1 payments, negotiate Tier 2 delays, cancel Tier 3 entirely, and use vendor communication scripts.

Vendor communication scripts that actually work

Proactive communication prevents most late payment consequences. Vendors prefer knowing about delays over surprised defaults. But most households avoid these calls from embarrassment or not knowing what to say.

For Tier 2 vendors during buffer shortage: "I'm calling about my account ending in [last 4 digits]. I'm self-employed and experiencing a temporary income delay. I can maintain service with a partial payment of [amount] on [date] and catch up the balance by [realistic date]. Can we arrange that to keep my account in good standing?"

Key elements: You called them (shows responsibility), specified the partial amount (shows commitment), provided a catch-up date (shows planning), requested "good standing" (protects credit).

For services you need to pause: "I need to temporarily suspend my service but want to maintain my account for reactivation. My work is seasonal and I'll need to restart service around [date]. What's the best way to pause without losing my account history or facing reactivation fees?"

This often reveals pause options not advertised. Many services offer holds, seasonal suspensions, or minimal maintenance plans to retain customers.

For one-time hardship assistance: "I've been a customer for [duration] and this is my first time having payment difficulty. My income varies as a [profession] and this month fell below projections. Do you have any one-time hardship programs that could help me maintain service? I expect normal income to resume by [date]."

Most utilities, insurance companies, and even some subscription services have unpublished hardship programs. You need to emphasize your history, explain the situation professionally, and show it's temporary.

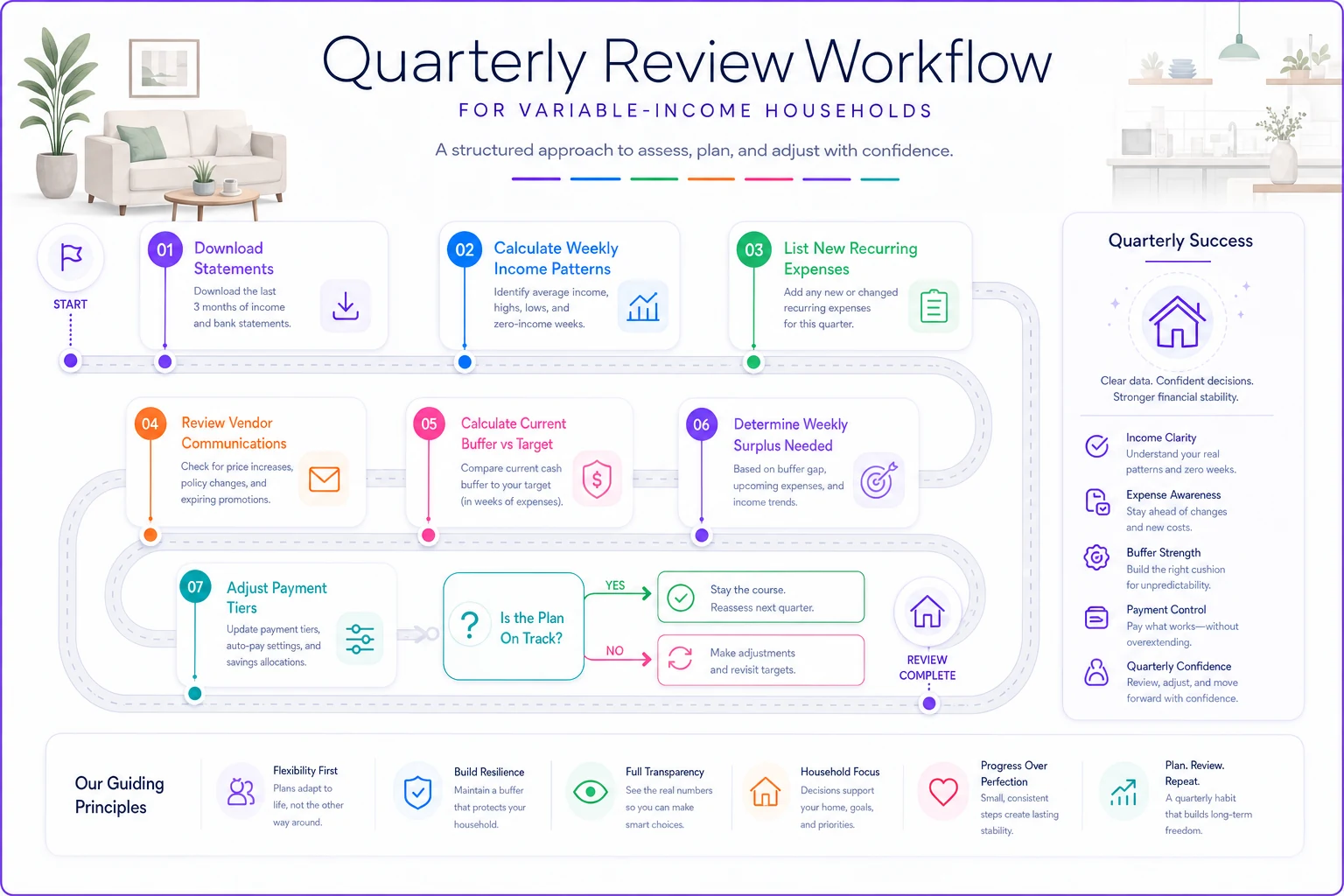

Quarterly workflows for variable income stability

Every three months, variable income households need specific operational reviews that steady-income households never consider.

Income pattern analysis: Pull three months of deposits. Calculate the weekly average, the lowest week, the highest week. More importantly, count the number of zero-income weeks. This reveals your real volatility, not the story you tell yourself.

A rideshare driver might discover they averaged $950 weekly but had four complete zero weeks when sick or taking breaks. That's different from believing "I make about $1,000 a week" and wondering why money feels tight.

Expense creep audit: List every Tier 3 expense added in the last quarter. Variable income households unconsciously add subscriptions during good periods that strangle cash flow later. That HBO Max subscription from a flush month becomes another $16 monthly obligation during lean times.

Vendor relationship documentation: Note which companies offered flexibility when you called. Which required no explanation? Which threatened immediate cutoff? This intelligence guides future payment prioritization. The internet company that offered a two-week extension moves up priority. The gym that demanded immediate payment drops lower.

Buffer rebuild planning: If your buffer dropped below target, calculate the weekly surplus needed to rebuild it within 90 days. If your target is $7,200 and you have $3,600, you need $40 weekly surplus for 90 days. That's specific enough to execute, versus vague "save more" intentions.

The quarterly review process follows this sequence:

-

Download three months of bank statements

-

Calculate actual weekly income patterns (including zero weeks)

-

List all new recurring expenses added during the quarter

-

Review vendor communication attempts and outcomes

-

Calculate current buffer level versus target

-

Determine weekly surplus needed for buffer rebuild

-

Adjust Tier rankings if priorities changed

A quick visual of the quarterly review steps can make the sequence easier to follow.

The mechanical difference this makes

A freelance photographer implementing this system watched their financial stress evaporate despite income varying from $1,800 to $7,000 monthly. Not through earning more or spending less, but through operational clarity.

Instead of checking their bank balance anxiously each morning, they check their buffer level weekly. Above target? Pay everything normally. Below target? Execute the established protocol. No decision fatigue, no panic, just mechanical execution of predetermined operations.

Their vendor relationships improved because companies prefer customers who communicate over those who ghost. Their credit improved because Tier 1 payments never arrived late. Their marriage improved because money discussions became operational rather than emotional.

The framework handles the volatility mechanically so you don't handle it emotionally. When income drops, you're not making stressed decisions about which bills matter most. You already decided that during calm periods.

When automation makes sense for variable income management

After operating this system manually for six months, patterns emerge showing where AI-powered operational software could help. Not as a replacement for understanding your finances, but as execution support once you know your patterns.

The manual system reveals which notifications matter (buffer dropping below 2x survival) versus which create noise (daily balance fluctuations). It shows which vendor communications happen repeatedly (internet company pause/resume) versus one-time events (insurance hardship request). It identifies which calculations waste mental energy (weekly buffer level checks) versus require human judgment (Tier ranking updates).

Operational platforms designed for variable income can monitor buffer levels continuously, alert when thresholds cross, queue vendor communications when needed, track payment hierarchies, and calculate survival numbers automatically. But these tools only work after you understand your actual patterns through manual operation first.

Software can automate the buffer calculations that currently require spreadsheet work. It can track which vendors respond well to payment flexibility versus those requiring immediate action. It can queue the right communication scripts when buffer levels drop below thresholds.

Most importantly, AI-powered systems can learn your specific income patterns and predict cash flow gaps before they arrive. Instead of reacting to low buffers, you get early warnings when projected income won't cover upcoming Tier 1 expenses.

The difference: you're automating a proven system, not hoping software solves undefined problems.

Stop fighting income variability and start operating with it

Traditional financial advice treats irregular income as a problem to solve through better budgeting. Income variability isn't going away though. The freelance economy keeps growing. Commission structures keep expanding. Side hustles keep multiplying.

Fighting variability with tools designed for stability creates unnecessary operational friction. Like forcing a river into a straight line instead of building proper channels for its natural flow.

The prioritized payment system, buffer management, and vendor communication protocols described here don't eliminate income variation. They create operational stability despite the variation. Your income still fluctuates. Your lifestyle still adjusts. But your core operations continue functioning regardless.

Variable income requires different financial operations, not better financial discipline. Build the right operational framework and the stress disappears even when the variability remains.

Variable income requires different financial operations, not better financial discipline. Build the right operational framework and the stress disappears even when the variability remains.

Ready to simplify your household management?

Join thousands of families using Famioly to save time, reduce home management stress, and keep the household running smoothly.